What Is FDIC Insurance? Your 2026 Protection Guide

What Is FDIC Insurance? Your 2026 Protection Guide !

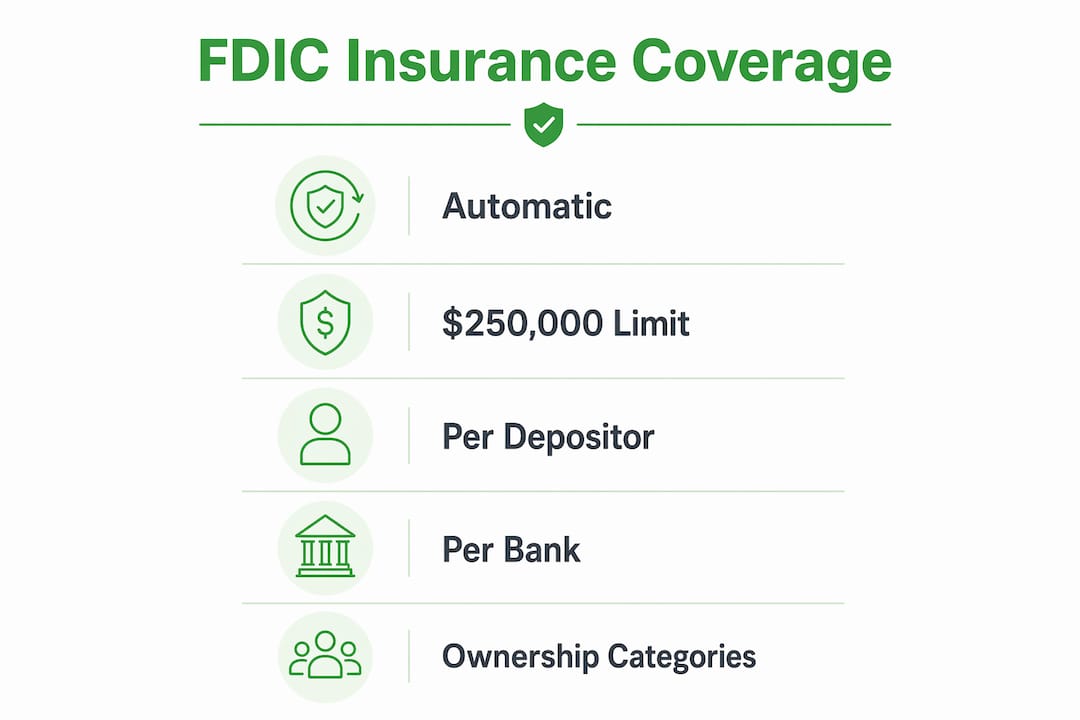

FDIC insurance is defined as a federal program that protects your bank deposits up to $250,000 per depositor, per insured bank, per ownership category if your bank fails. The Federal Deposit Insurance Corporation has backed American depositors since 1934, and no depositor has lost insured funds in that entire span. Coverage is automatic. You pay nothing for it. Your bank pays the premiums, not you. For individuals and families building financial security, understanding what is FDIC insurance and how it works is the foundation of safe banking.

What is FDIC insurance and what does it cover?

FDIC insurance covers deposit accounts held at FDIC-insured institutions, which number over 4,000 banks across the United States as of 2026. That number represents the breadth of the program’s reach. If your bank carries the FDIC label, your eligible deposits are protected automatically from the moment you open an account.

The following account types are covered under FDIC insurance:

- Checking accounts — standard personal and business checking

- Savings accounts — including high-yield savings accounts at FDIC-insured banks

- Money market deposit accounts — bank-issued accounts, not money market mutual funds

- Certificates of deposit (CDs) — you can use a CD interest calculator to estimate returns on these insured products

- Cashier’s checks and money orders issued by the bank

What FDIC insurance does not cover is equally important to understand. The following products are explicitly excluded, regardless of where you purchase them:

- Stocks, bonds, and mutual funds

- Cryptocurrency assets

- Life insurance policies and annuities

- Safe deposit box contents

- Treasury securities purchased directly through the U.S. Treasury

These exclusions are defined by the FDIC and apply universally. A brokerage account at a bank branch is not a deposit account. It does not qualify. This distinction catches many depositors off guard, particularly those who hold investment products at the same institution where they bank.

Pro Tip: If you are unsure whether a specific product at your bank is FDIC-insured, ask the bank directly for written confirmation. The FDIC’s BankFind tool at fdic.gov also lets you verify any institution’s insured status in seconds.

How does FDIC insurance work when a bank fails?

When a bank fails, the FDIC steps in as the receiver and takes control of the institution’s assets and liabilities. The process moves quickly. Insured deposits are typically restored within one to two business days, either by transferring your account to an acquiring bank or by issuing a direct payment. Most depositors experience little to no disruption.

Here is the sequence of events when a bank closes:

- Regulators close the bank and appoint the FDIC as receiver, usually on a Friday evening.

- The FDIC identifies an acquiring bank to assume insured deposits, or prepares direct reimbursement checks if no acquirer is found.

- Depositors gain access to their funds by the next business day in most cases, through the acquiring institution or a mailed check.

- The FDIC sells the failed bank’s assets to recover funds and pay creditors, with insured depositors receiving priority.

One detail that surprises most people: the FDIC fund is financed entirely by bank premiums and interest on investments. Congress does not appropriate money to the FDIC. Taxpayers do not fund it. This independence strengthens the program’s reliability because its resources are not subject to annual budget negotiations.

“The FDIC’s supervisory role helps identify risks early, contributing to an overall safe banking environment.” — FDIC.gov

The FDIC also supervises over 2,700 banks for safety and soundness, which means it works to prevent failures before they happen. The insurance function and the supervisory function work together. Fewer failures mean fewer claims against the fund.

How FDIC insurance coverage limits and ownership categories work

The $250,000 limit is not a ceiling for your total coverage across all accounts. It is a ceiling per depositor, per bank, per ownership category. That distinction matters enormously for families with significant deposits.

The FDIC recognizes several ownership categories, each with its own $250,000 limit:

| Ownership category | Coverage limit | Example |

|---|---|---|

| Single account | $250,000 | One person, one bank |

| Joint account | $250,000 per co-owner | Two owners = $500,000 total |

| IRA or retirement account | $250,000 | Separate from other accounts |

| Revocable trust account | $250,000 per beneficiary | Four beneficiaries = $1,000,000 |

| Employee benefit plan | $250,000 per participant | Applies to certain pension accounts |

A married couple with a joint checking account, individual savings accounts, and IRAs at the same bank could have well over $1,000,000 in fully insured deposits. Spreading funds across ownership categories and multiple FDIC-insured banks is a recognized strategy for depositors who need coverage beyond the standard limit.

In rare cases involving systemic financial risk, federal authorities can extend coverage beyond standard limits. The 2023 Silicon Valley Bank intervention is the clearest recent example. Treasury Secretary Yellen invoked the systemic risk exception to cover all deposits, including those above $250,000. That decision was extraordinary and not a standard feature of FDIC insurance. Depositors should not plan around it.

Pro Tip: The FDIC offers a free online tool called EDIE (Electronic Deposit Insurance Estimator) at fdic.gov. Enter your account details and it calculates your exact coverage across all ownership categories at a given bank. Use it before you exceed the $250,000 threshold.

Common misconceptions about what FDIC insurance does not protect

FDIC insurance is powerful, but it has clear limits that many depositors misunderstand. The most common misconception is that FDIC insurance protects against all financial losses at a bank. It does not.

The program covers deposit balances up to the insured limit if the bank fails. It does not cover:

- Fraud or theft losses — if someone steals from your account, that falls under federal Regulation E, not FDIC insurance. Unauthorized transaction losses are governed by separate consumer protection rules.

- Investment losses — a CD that matures at a lower rate than expected is not an FDIC claim. Market performance is outside the program’s scope.

- Deposits above the insured limit — if you hold $400,000 in a single account at one bank, $150,000 is uninsured and at risk in a failure.

- Non-bank financial institutions — credit unions use a separate program called NCUA insurance. Fintech apps that hold funds at partner banks may or may not pass through FDIC coverage depending on their structure.

About 39% of U.S. deposits were uninsured as of March 2025, primarily because balances exceeded the $250,000 limit or were held at non-insured institutions. That figure represents real financial exposure for households and businesses that have not reviewed their account structures. The solution is straightforward: use multiple ownership categories, multiple banks, or both.

Vanguard emphasizes FDIC insurance as a cornerstone of conservative cash management, particularly for emergency funds and short-term savings. Keeping liquid cash in FDIC-insured accounts and investing separately through brokerage accounts is the standard approach for households that want both growth and protection.

Key takeaways

FDIC insurance protects up to $250,000 per depositor, per bank, per ownership category automatically, at no cost to you, and no depositor has lost insured funds since 1934.

| Point | Details |

|---|---|

| Coverage is automatic | No enrollment or fees required; your bank pays the premiums on your behalf. |

| Covered account types | Checking, savings, money market deposit accounts, and CDs are all protected. |

| Ownership categories multiply coverage | Joint accounts, IRAs, and trusts each carry separate $250,000 limits. |

| Investments are not covered | Stocks, bonds, crypto, and annuities fall outside FDIC protection entirely. |

| 39% of deposits are uninsured | Balances above limits or held at non-insured institutions carry real risk. |

Why most families are underprotected and don’t know it

I have spent years watching people assume their money is safe simply because it sits in a bank. That assumption is mostly correct, but the gap between “mostly” and “fully” is where real financial damage happens.

The families I see most at risk are not reckless. They are savers. They accumulate cash in a single savings account over years, cross the $250,000 threshold without noticing, and never think to restructure. The FDIC’s own data showing that 39% of U.S. deposits remain uninsured confirms this is not a fringe problem.

What I find equally underappreciated is the ownership category system. Most people treat it as a technicality. It is actually one of the most practical tools in personal finance. A couple with a joint account, two individual accounts, and two IRAs at the same bank has five separate coverage buckets. That is $1.25 million in potential coverage at a single institution, with no additional cost or complexity.

My honest recommendation: review your account structures once a year, the same way you review your insurance policies. Use the FDIC’s EDIE tool. If you are approaching the limit in any single category, open an account at a second FDIC-insured bank or restructure into a trust account. Experts consistently recommend this periodic review as part of sound cash management. It takes thirty minutes and it protects everything you have saved.

Bank with confidence through Rmous

Rmous offers FDIC-insured checking and savings accounts designed for individuals and families who want security alongside everyday convenience. Every deposit account at Rmous carries full FDIC coverage automatically, so your money is protected from the moment you open an account.

Beyond deposit protection, Rmous members access a connected financial ecosystem that includes loans, insurance, and RMOPay™ for instant member-to-member transfers. The MyRMO digital banking platform gives you at-a-glance account management with the security of biometric authentication. If you want a banking relationship that combines FDIC protection with real member benefits, Rmous is built for exactly that. Visit rmous.org to explore your options.

FAQ

What is the FDIC insurance limit per account?

FDIC insurance covers up to $250,000 per depositor, per insured bank, per ownership category. This limit has been permanent since 2010.

Does FDIC insurance cover all deposits automatically?

Yes. Coverage is automatic for eligible deposit accounts at FDIC-insured banks. No enrollment or application is required, and depositors pay no fees.

What accounts are not covered by FDIC insurance?

Stocks, bonds, mutual funds, cryptocurrency, life insurance policies, annuities, and safe deposit box contents are all excluded from FDIC coverage.

How quickly do you get your money if a bank fails?

The FDIC typically restores access to insured deposits within one to two business days after a bank failure, either through an acquiring bank or direct payment.

Can you have more than $250,000 in FDIC coverage at one bank?

Yes. By using different ownership categories such as joint accounts, IRAs, and revocable trusts, a depositor can hold well over $250,000 in fully insured deposits at a single FDIC-insured institution.